Find Your DREAM home!

Atlanta’s Hot Properties

View a few choice homes & land.

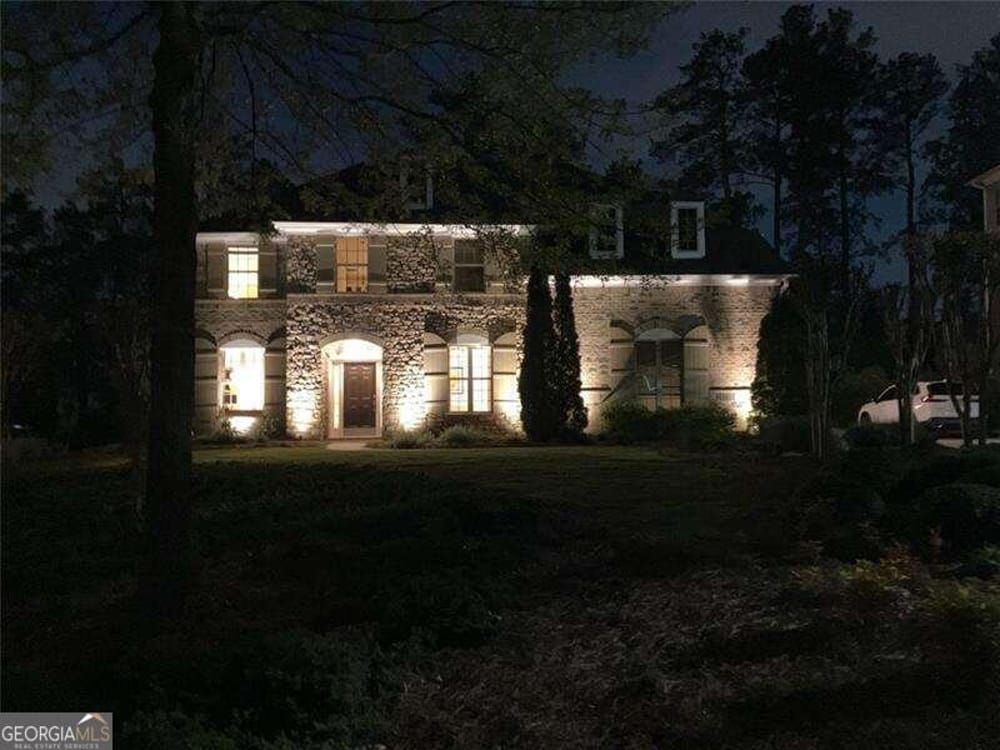

New - 5,978 Hours

Open House

Virtual Tour

Price Drop

(237d)

4 bd

3 ba

913 Andover Court, Woodstock, GA 30188

Listing Courtesy Of: Keller Williams Realty Community Partners, Michael Hickman, First MLS

New - 140 Hours

Open House

Virtual Tour

6 bd

6 ba

3037 Towerview, Atlanta, GA 30324

Listing Courtesy Of: Ansley Real Estate | Christie's International Real Estate, 404-358-4522, Cliff Miller, First MLS

New - 3 Hours

Open House

Virtual Tour

4 bd

3 ba

2469 Ellis, Snellville, GA 30078

Listing Courtesy Of: Virtual Properties Realty. Biz, Alejandro Bonilla, First MLS

New - 27 Hours

Open House

Virtual Tour

5 bd

3 ba

6585 Springfield, Atlanta, GA 30331

Listing Courtesy Of: Compass, Ashley Sellers, First MLS

New - 97 Hours

Open House

Virtual Tour

Price Drop

(1d)

5 bd

3 ba

128 Windfields, Woodstock, GA 30188

New - 21 Hours

Open House

Virtual Tour

4 bd

3 ba

885 Highland, Marietta, GA 30066

Listing Courtesy Of: Peachtree Property Residential, LLC, [email protected], Hardeman Team, First MLS

New - 526 Hours

Open House

Virtual Tour

Price Drop

(1d)

5137 Yellow Stone, Flowery Branch, GA 30542

Listing Courtesy Of: Century 21 Results, Dany Drouin, First MLS

New - 2,068 Hours

Open House

Virtual Tour

6 bd

8 ba

5070 Lake Forrest Dr, Sandy Springs, GA 30342

Listing Courtesy Of: Atlanta Fine Homes Sotheby's International, Bonnie Majher, First MLS

New - 21 Hours

Open House

Virtual Tour

5 bd

5 ba

1145 Tennyson, Brookhaven, GA 30319

Listing Courtesy Of: Ansley Real Estate | Christie's International Real Estate, Bonneau Ansley Iii, First MLS

New - 99 Hours

Open House

Virtual Tour

3 bd

3 ba

120 Batten Board, Woodstock, GA 30189

Listing Courtesy Of: Compass, Minhnuyet Hardy, First MLS

My Blog (Buyers Guide)

Explore our blog posts to learn from the best about buying selling and maintaining your home

Contact Me